We build and operate top-tier tech teams in LATAM and Eastern Europe.

Up to 40% savings. 100 people a year. No entity. No buy-out fees.

The Employer of Record vs Permanent Establishment question often catches expanding US tech companies off guard. In short, Permanent Establishment (PE) refers to a fixed place of business or significant local activity in a foreign country substantial enough to trigger corporate tax liability, such as back-taxes, penalties, and mandatory local registration. Meanwhile, an EOR is the legal employer – not the source of that risk. Your employees’ roles, authority, location, and in-country activity usually are.

As a tech-exclusive Employer of Record with zero PE cases across our entire client base, Alcor will ensure PE-risk-free expansion of your business in LATAM or Eastern Europe. We scale teams from 0 to 30 senior engineers in 3 months, with full coverage from the first CV to your owned tech R&D center.

Read this article to learn more about what actually triggers PE, how EOR structurally reduces it, and where the model’s limits are to protect your expansion before the exposure quietly builds into a bill.

Key Takeaways

- Permanent establishment is not triggered by an EOR itself. PE risk arises when a foreign company establishes sufficient business substance in another country through local premises, senior decision-making, sales activity, contract authority, or employees acting on its behalf.

- The main PE triggers for tech companies include recurring home offices or co-working spaces, employees who negotiate or effectively close contracts, local work tied to revenue generation, long-term in-country presence, and senior leaders operating from another jurisdiction.

- An Employer of Record helps reduce PE risk by separating the local employment layer from the client’s legal entity. The EOR handles employment contracts, payroll, statutory benefits, tax withholding, and local HR records, while the client must still control employee authority, reporting lines, work locations, and documentation.

- Alcor helps US and European tech companies scale engineering teams in LATAM and Eastern Europe, minimizing PE exposure through its legal shield, owned legal entities, compliant contracts, payroll and benefits administration, and IP protection. Beyond EOR, Alcor covers tech recruitment and ops support, which enables fast team scaling while avoiding vendor sprawl and overpayment.

What is Permanent Establishment and What are Its Consequences?

A Permanent Establishment is a sufficient business presence of a company in a foreign country to trigger tax liability on profits generated by its activity.

PE can be triggered by local premises, remote work locations, senior decision-makers, sales activity, or employees acting on your behalf.

The consequences can include back taxes, penalties, local registration duties, additional compliance obligations, double taxation risks, and reputational damage.

Permanent Establishment is when your tech company has enough business presence in a foreign country for local tax authorities to tax your profits linked to that activity. For tech companies, PE risk can come from local premises, senior decision-makers, sales or business development roles, or employees who regularly act on the company’s behalf.

A KPMG global survey found that 65% of companies cite PE risk as a primary compliance challenge in international remote work. And it’s no wonder, as traditionally PE required a physical building, such as an office or factory. But in today’s world, remote work has made the picture less tidy. A home office, co-working space, or other recurring work location can become relevant when an employee carries out business activities there with enough permanence and substance.

The OECD’s November 2025 update to the Model Tax Convention clarifies when cross-border work-from-home may create a fixed-place PE. One important benchmark is the 50% working-time test. If an employee works from a foreign home address for more than half of their total working time, that address can be treated as your company’s place of business.

Still, it doesn’t automatically mean that your company is under PE risk. Tax authorities look at the facts: what the employee does, whether the work is continuous, whether the company has a commercial reason to have that person physically located in the country, and whether the activities are core to the business or merely auxiliary.

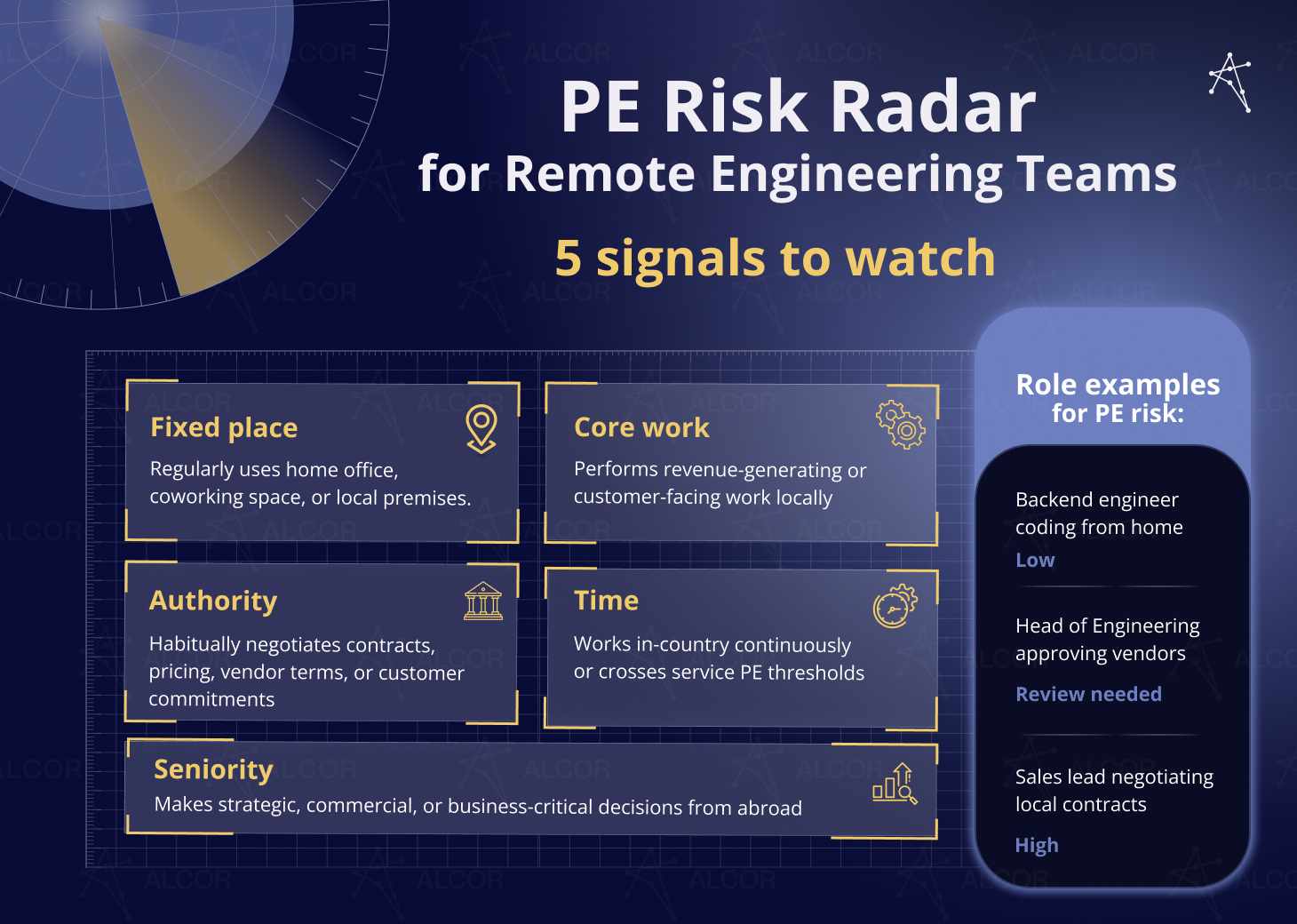

For more context: a Backend Engineer in Warsaw working only on internal product tasks may create a different risk profile than a senior leader in Bogotá negotiating with local partners, managing customer delivery, or providing real-time support to customers in that region.

While I’ll discuss the key PE triggers in more detail in the next chapter, it’s worth mentioning possible consequences of the PE risk. There are three primary categories:

- Financial consequences such as back taxes on profits attributed to the PE, with interest applied retroactively. Plus, additional financial penalties, the severity of which depends on the bilateral treaty between your home country and the host jurisdiction and, in some cases, on whether the PE was created knowingly. In some countries, permanent establishment corporate tax, VAT, and social security can be applied.

- Legal and operational consequences associated with local business registration obligations, full compliance with host-country employment and labor law, and a formal corporate filing structure. Double taxation could also be the case if your home country and the host country both assert the right to tax the same profits.

- Reputational, especially for companies trying to scale internationally. Being found to have avoided local taxes, even unintentionally, damages relationships with regulators, complicates future hiring in the same market, and creates friction with the engineers you’re counting on to stay.

The biggest problem with permanent establishment risk is that it usually compounds quietly. By the time a tax authority asks questions, the activity may have been happening for months or years. That is why PE should be treated as an early-stage expansion risk. Knowing how to avoid permanent establishment risk before hiring abroad is much easier than explaining two years of local activity to a tax authority later.

5 Key Permanent Establishment Triggers

When expanding your operations abroad, tech companies should consider these main PE risk triggers:

- use of local premises or remote home offices;

- employees negotiating or effectively closing contracts;

- local work tied to revenue or core value creation;

- duration, continuity, and service PE thresholds;

- senior leaders or market-facing roles operating from another country.

An EOR keeps employment, payroll, and local HR compliance clean. But PE risk follows what your people actually do – not what the contract calls them.

1. Fixed place of business and use of premises

It’s the oldest and most intuitive trigger: your company has a physical location in a foreign country that it uses to conduct business. This may be an office, a server room, or a dedicated co-working membership in a shared space your team regularly occupies. All of these examples can qualify as a fixed place under Article 5(1) of the OECD Model Tax Convention if they meet three conditions: the location is specific, the company has it at its disposal, and its use is ongoing rather than occasional.

What changed in November 2025 is the way tax authorities may look at home offices. The OECD’s updated Commentary to Article 5 introduced a framework for evaluating when a remote worker’s home address becomes your company’s fixed place of business, including two key indicators:

- Working time: if the employee works from that address for more than 50% of their total working time over a 12-month period, the location clears the “fixed” threshold.

- Commercial reason: if the employee’s presence in that country serves a genuine business purpose. This could be direct customer or supplier interaction, local market development, access to business-relevant expertise, or real-time support across time zones.

In most cases, both working time and commercial reasons are necessary to trigger fixed-place PE. Still, the analysis remains fact-specific. For example, an engineer working remotely from Bucharest because they prefer living there, with no local clients, no market-facing role, and no business reason for the company to have them in Romania, does not automatically create PE exposure under the updated OECD framework. But a developer based in Warsaw who works full-time from home, supports European customers in real time, and performs a function that is core to the company’s business may look different to a Polish tax authority.

2. Dependent agents who negotiate or conclude contracts

Now, moving to the least forgiving PE trigger and one of the most relevant risks to review in an EOR arrangement.

Under Article 5(5) of the OECD Model, a permanent establishment can exist when a person habitually acts on behalf of a foreign company and either concludes contracts in its name or plays the principal role leading to their conclusion. The key word is “habitually.” A one-off transaction usually does not meet the threshold. But a sales lead who regularly negotiates pricing, scopes agreements, aligns commercial terms, and passes contracts to headquarters for a formality signature can create a very different risk profile.

Post-BEPS Action 7, the standard was deliberately tightened. The pre-2017 version covered agents who signed contracts. The revised language captures anyone who drives the deal to conclusion, even if the ink goes on paper at headquarters. A foreign employee who negotiates all material terms while headquarters rubber-stamps the result is, in the eyes of most tax authorities, functionally concluding that contract locally.

The distinction between “playing a role in negotiations” and “habitually concluding contracts” is critical under the OECD framework. The former is generally safe. The latter creates EOR PE risk regardless of what the employment contract says. Tax authorities don’t read org charts. They trace what the person actually did. This is why role design matters as much as legal structure.

3. Revenue-generating or core business activities carried out locally

Many tax treaties exclude activities that are genuinely preparatory or auxiliary from PE classification. Think market research, attending industry events, collecting information, or internal support work that does not form a core part of how the company makes money. But after BEPS Action 7, this protection became narrower. Activities that once looked “supportive” can lose that status if they are now essential to the company’s business model.

The hard part is the line between support and core value creation. That’s where tax authorities pay attention to what the person actually does, how important that work is to the company’s business, and whether the company is effectively carrying on business in the country through that activity.

You may say, “But I hire my talent through an EOR, so it’s not a problem.” Yes, in an EOR arrangement, the provider acts as the legal employer of the worker in the target country. But the EOR does not completely eliminate PE risk for the client company. If workers hired through an EOR perform activities on behalf of the client that go beyond preparatory or auxiliary support, the arrangement may still create tax exposure. This is where Employer of Record tax implications become harder to contain.

For tech product companies, this shows up in a specific way. Most jurisdictions don’t treat product engineering as a PE trigger on its own because the engineers don’t sell anything locally. But add local client delivery, direct customer-facing work, or IP creation that generates revenue abroad, and the picture may shift.

4. Duration, continuity, and habitual presence

Many bilateral tax treaties include a service PE threshold. This means a foreign company may create a permanent establishment if its employees or other personnel provide services in a country for more than a defined number of days. The commonly cited benchmark is 183 days (roughly 6 months) within a 12-month period, especially in treaties influenced by the UN Model.

The counting method also depends on the treaty and local interpretation. In some cases, days are counted across employees working on the same or connected project. In others, overlapping days may not be double-counted. So three engineers spending 70 days in-country each may or may not cross the threshold, depending on whether their days overlap, what services they perform, and how the relevant treaty counts presence.

The 183-day rule is widely known but often misunderstood. Days do not always need to be consecutive. A short return home does not necessarily reset the clock if the treaty looks at any rolling 12-month period. And depending on the country, partial days or business travel days may count – though some service PE cases focus only on days when services are actually performed in the country.

Continuity matters beyond day counts, too. For fixed-place PE, the OECD framework does not require activity to be permanent in the sense of never stopping. Operations must be carried out on a regular basis. A location used for short periods but repeatedly over a long period may still create PE exposure if the company has that place at its disposal and carries on business through it.

5. Senior management, country leadership, and market-facing roles

The more authority a person has, the higher the PE exposure can become – not because seniority itself is the trigger, but because senior people make decisions, represent the company, and often shape commercial outcomes. That is exactly the kind of substance tax authorities examine when deciding whether a foreign company is carrying on business in their jurisdiction.

A VP of Engineering, country director, or senior executive working from a foreign location creates a different risk profile than a mid-level developer doing the same. Senior leaders set strategy, manage teams, approve budgets, represent the company to partners or customers, and may have explicit or implicit authority to commit the organization to business decisions.

Risks increase further if the worker has authority to negotiate or conclude contracts, or habitually plays the principal role, resulting in contracts that the company approves without meaningful changes. An example of a head of engineering is relevant here. If they consistently run sprint planning, approve vendor contracts, represent the company in technical due diligence, and make business-critical delivery decisions from a foreign address, it may also deserve a closer PE review.

This is where EOR contract clauses and PE protections have hard limits. An EOR can structure employment compliantly and keep payroll clean. But it cannot change what a senior leader does while in-country.

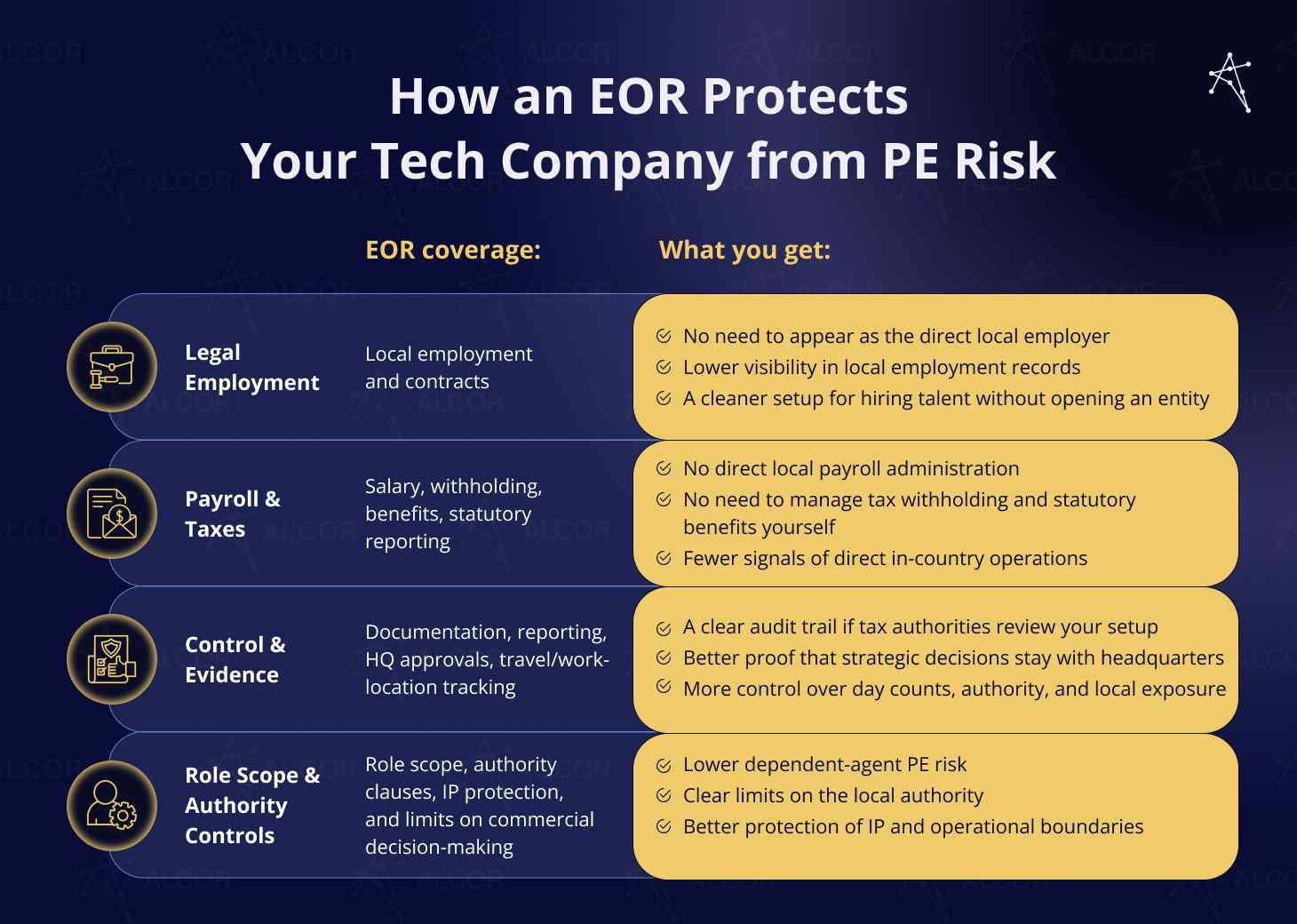

How an Employer of Record Mitigates PE Risk

An Employer of Record helps you mitigate PE risk by keeping the local employment layer separate from your company’s legal entity. The EOR becomes the legal employer, signs local contracts, runs payroll, handles tax withholding, statutory benefits, and employment documentation.

This reduces your visible local footprint. But it doesn’t remove PE risk completely. You still need to control:

- What your employees do locally;

- Whether they can negotiate or close contracts;

- Where decisions are made;

- How reporting lines and documentation are structured.

Start EOR permanent establishment risk review before hiring. The safest setup combines a compliant employment structure with clear role boundaries, centralized decision-making, and documentation that matches daily operations.

Legal employment separation and local contracting structure

The foundation of mitigating PE risk with EOR is simple: the EOR becomes the legal employer of your engineers in the foreign country. It signs the local employment contract, runs payroll, handles statutory benefits, and manages employer-side tax and social security obligations. Meanwhile, your company works with the EOR through a separate service agreement. This means you can hire and manage talent abroad without your company appearing directly in the documentation as the local employer.

That separation matters. PE risk often increases when a foreign company starts building a visible local footprint. A properly structured EOR arrangement helps reduce it, so that the local employment layer sits with the EOR’s entity, not with you. For a US tech company hiring engineers abroad, this can be a meaningful protection. You get a compliant way to employ local talent without setting up your own legal entity, registering as a local employer, or building payroll infrastructure from scratch.

That’s what Dotmatics, a US scientific software company, got when expanding its engineering team into Eastern Europe. Alcro’s EOR solution covered:

- Employment contracts tailored to local labor laws and the GDPR, including IP protections.

- Payroll processing and remuneration remittance handled through Alcor’s own legal entity

- Onboarding within defined SLAs, including equipment procurement

- Stock option payouts were paid in full to all engineers when Siemens acquired Dotmatics.

Dotmatics built a truly integrated 30-engineer team without any entity, compliance, or PE troubles in Eastern Europe.

Local payroll, tax withholding, and statutory compliance

Beyond employment structure, the way money moves plays a role. If your US-based tech company pays local workers directly, manages salary withholding, or handles social security contributions itself, it creates a visible local employment and tax footprint. That does not automatically create PE, but it can raise questions about whether your company is operating in the country more directly than intended.

This is where an EOR adds practical protection. Your local provider handles everything from salary payments, income tax withholding, to health insurance, pension enrollment, mandatory benefits, and statutory reporting to local authorities. Meanwhile, you just pay a consolidated service invoice and focus on building the software product.

This matters for Employer of Record tax implications in two ways:

- It ensures the employment relationship is fully visible and compliant with local authorities, which reduces the kind of scrutiny that leads to broader PE investigations.

- It means your company has no direct tax registration, no local filing obligations, and no admin presence in the jurisdiction. Those are exactly the signals that trigger corporate tax assessments.

For country-specific expansion planning across LATAM, compare the best Employer of Record in Mexico and the best Employer of Record in Colombia to select the optimal partner.

Limiting employee authority and role design to avoid agency risks

Legal separation and clean payroll do reduce admin exposure. But as I’ve mentioned previously, they don’t change what your employee actually does in the country where you’re expanding. In this case, EOR structure alone will not prevent dependent-agent PE risk. Tax authorities look at commercial reality, not just contract labels.

Mitigating PE risk with EOR means defining what locally employed developers are authorized to do before the role goes live. For engineering teams, this is usually straightforward: building software, reviewing code, attending standups. None of that creates dependent agent exposure. The risk rises when the role becomes client-facing, commercial, or decision-heavy.

That’s why contract clauses matter. A well-structured EOR agreement can define the employee’s scope, clarify that the EOR is the legal employer, and limit the worker’s authority to bind the client company. But it’s essential to remember that contract language only works if it matches operational reality. The practical approach is to map every EOR role against dependent-agent PE criteria before hiring and revisit that mapping as the role evolves.

Centralized control, reporting lines, and documentation practices

Structure and role design reduce PE risk. Documentation helps prove that the structure works in practice. Apart from the contract, tax authorities also pay attention to how the organization actually functions: reporting lines, decision-making trails, email records, signed contracts, travel patterns, and who had authority over what. To avoid PE risk, make sure you have these aspects sorted out well:

- Reporting lines should stay clearly connected to headquarters. This means that strategic decisions, such as product direction, commercial commitments, pricing, and major vendor approvals, should be traceable to decision-makers in the home jurisdiction.

- Track day counts and work locations as a policy. This is especially important for senior leaders, frequent travelers, and employees whose roles involve customers, partners, or commercial decisions.

- Your documentation needs to stay current, so you would have solid evidence in the event of a dispute. Employment contracts, EOR service agreements, role descriptions, org charts, payroll records, authority limits, travel logs, and approval workflows should all tell the same story. If an employee’s role, compensation, reporting line, location, or authority changes, the records should change too.

This is where an EOR partner comes in handy by taking care of local filings, statutory records, and employment documentation, while you stay responsible for the operational layer.

Common High-risk Scenarios That Create PE Exposure

Common high-risk PE scenarios appear when your local team starts acting less like remote talent and more like your company’s business presence in the country. This may happen when developers negotiate vendor terms, manage local engineering operations, work from dedicated premises, or fall under stricter domestic PE rules than the treaty suggests. In these cases, clean EOR or COR contracts may not be enough if the real work looks commercial, managerial, or market-facing.

Alcor’s approach is to reduce this exposure through clear role scope, local engagement structure, authority limits, documentation, and separation between technical execution and strategic or commercial decision-making.

When dependent-agent rules override contractual arrangements

| Your platform engineering lead in Warsaw manages vendor relationships for third-party infrastructure: cloud providers, data pipeline tools, security audits. Over time, they’ve started negotiating renewal terms directly. Nothing gets signed without a San Francisco countersignature, but every commercial parameter is set in Warsaw first. |

Possible consequence: Poland opens a corporate tax inquiry. A profit attribution exercise determines what share of vendor-driven activity is attributable to local operations, and taxes it retroactively at 19%, plus interest, potentially back to day one of the engineer’s tenure.

Alcor’s approach: Alcor helps reduce dependent-agent PE risk by creating a clearer separation between your core business decisions and the local operational layer from the start. This means keeping the local role limited to technical work, vendor assessment, and internal recommendations – not commercial negotiations or deal-making. For higher-risk roles, Alcor can also help companies review the scope before hiring and flag functions that may look too commercial, management-heavy, or client-facing.

Economic nexus from sales or revenue attribution

|

Your three solutions engineers in Kyiv handle all European enterprise pre-sales: technical qualification calls, product demos, RFP responses, security architecture reviews. They don’t sign anything. But they are the reason European deals close. |

Possible consequence: A revenue attribution finding in a high-enforcement jurisdiction, or a country applying SEP rules, means corporate tax is assessed on the portion of European ARR your local solutions team demonstrably drove, calculated retroactively from when the pattern of activity began.

Alcor’s approach: Alcor helps reduce this risk by structuring local specialists as technical contributors, not revenue-driving representatives of the client company. In this case, the solutions engineers in Kyiv can support demos, answer architecture questions, review security requirements, and help the HQ sales team understand technical fit. Alcor’s Contractor of Record (COR) model helps formalize this separation through role scope, documentation, and engagement structure.

Risks from in-country engineering leadership

|

Your Head of Engineering relocates to Bucharest to lead your 20-person Romanian team closer to the ground. They’re employed through the same EOR as the rest of the team. Within months, they’re running sprint planning, managing vendor SLAs, attending client technical reviews, and working from a dedicated co-working space five days a week. |

Possible consequence: A PE finding triggers retroactive profit attribution at Romania’s 16% corporate tax rate for activity attributable to the local engineering function. The broader tax residency and PE implications can be more severe: full Romanian corporate tax liability as a locally tax-resident entity, not a slice of attributed profit.

Alcor’s approach: Alcor helps reduce this risk by separating local team coordination from strategic company management. In this case, a Romanian-based engineering leader could support delivery, mentor engineers, and coordinate technical execution. But core decisions, like roadmap ownership or client-facing technical commitments, would remain with the client’s authorized leadership outside Romania.

A similar approach worked for Ledger, where Alcor helped hire QA and Delivery Managers in Eastern Europe while supporting legal and operational layers.

Alcor can also help structure the local setup so it does not default to looking like the client’s own Romanian office. This includes reviewing the role scope, avoiding unnecessary dedicated workspace, keeping vendor and client authority outside the country, and documenting that local activity is technical execution rather than local business management.

Jurisdictional exceptions and treaty-specific interpretations

|

You’re hiring backend engineers in Colombia. It’s your first LATAM footprint. Legal confirms the US-Colombia tax treaty. The OECD framework applies. Remote engineers, no client-facing work, clean EOR. Two years in, a Colombian tax authority inquiry arrives, citing domestic PE rules that are stricter than the treaty definition. |

Possible consequence: Even a remote engineering team with no commercial activity can trigger a service PE under domestic rules that deviate from the applicable treaty, resulting in back taxes, penalties, and mandatory local registration in a jurisdiction the company wasn’t prepared to operate in.

Alcor’s approach: With Alcor’s Contractor of Record model, clients can engage Colombian developers on a B2B basis while keeping the setup cleaner: contractors issue proper invoices, maintain independent tax compliance, use their own equipment where possible, and avoid employee-like benefits or authority. Their role should stay focused on product development and internal technical delivery – not customer management, local representation, or commercial decision-making.

Note: EOR and COR models do not completely eliminate PE risk. They act as a structural buffer by separating local talent engagement from the client’s direct local presence. But PE exposure still depends on the team’s actual activities, authority, duration, and commercial role in the country.

When to Establish a Local Entity Instead of Relying on an EOR

You should consider setting up a local entity when the country is no longer just a hiring location but a strategic business base.

This usually happens when you need:

- a large or long-term team with local leadership;

- local bank accounts, assets, procurement, or contracts under your company’s name;

- licenses, approvals, or regulated sign-off in-country;

- local invoicing, transfer-pricing setup, or access to tax incentives.

An EOR is great for testing and scaling fast. A local entity makes more sense when you need deeper control, commercial presence, and long-term infrastructure.

Scale, control, and strategic market considerations

An EOR works well when you are testing new markets, hiring the first few engineers, or building a distributed team without committing to a full local setup. But once the country becomes a strategic engineering hub, a local leadership layer, or a market-facing function, entity setup may make more sense.

Headcount still matters in this context, but it should not drive the decision alone. A 30-person engineering team building a software product under centralized decision-making may still fit well under a properly structured EOR model. A smaller team with a country lead, local customer relationships, commercial authority, or regulated responsibilities may justify an entity much earlier.

Control is the second factor. An EOR gives you a fast and compliant employment structure while keeping your team under your direct management. But if you need to open local bank accounts, sign contracts in-country, hold local assets, run local procurement under your own name, or build a visible long-term market presence, a local entity may eventually become the cleaner operating model.

Many scaling companies use both models as part of a broader global expansion strategy: an owned entity in their primary market where headcount justifies it, and EOR services in countries where local presence doesn’t yet warrant full entity setup.

For Alcor clients, the transition is designed to be operationally non-disruptive. Engineers hired through our EOR model can be transferred to the client’s own entity after six months, with no buyout fee, no vendor layer, and complete IP ownership from day one. See how our solution worked for your tech peers:

Regulatory, licensing, or sector-specific requirements

In certain cases, local regulations may make EOR legally impermissible as an employment structure. This could be applicable for companies in telecom, pharma, or financial services, which often need a registered local legal entity to hold the licenses required to operate. The EOR only handles the employment layer. It cannot hold a payment institution license, a securities dealer registration, or a data processing certification that the regulatory authority issues to a legal person. Those must belong to your entity.

So, how do you know if this is the case for your company? If the role your employee performs requires the company to hold a local license, authorization, or regulatory approval in order for that work to be legally conducted in-country, then an EOR is not sufficient. For example, a fraud engineer building detection models carries no licensing implications. A compliance officer with sign-off authority on regulated financial transactions is a different matter entirely. Roles requiring regulated sign-off or statutory local approvals and executives with in-country contract-signing authority are better suited to a directly owned entity.

Data regulation adds another layer. GDPR does not automatically require a company to create a local EU entity. However, companies processing EU personal data may need to comply with GDPR territorial-scope rules, appoint an EU representative in some cases, manage cross-border data transfers, and meet sector-specific data governance requirements.

Start scaling in Eastern Europe with full compliance from day one. See how Alcor helped BigCommerce scale its team to 50 engineers through a dedicated GDPR solution.

Long-term tax planning, transfer pricing, and commercial needs

Partnering with an EOR provider simplifies your employment and tax setup. That simplicity is a major advantage early on. But as your team becomes larger, more permanent, and more strategic, a local entity can unlock tools the EOR model is not designed to provide.

A registered subsidiary can support intercompany agreements, transfer-pricing documentation, cost-sharing or cost-plus R&D models, local invoicing, asset ownership, and access to tax incentives available only to qualifying local taxpayers. For tech companies, this can include regimes such as Poland’s IP Box or Ukraine’s Diia City, where eligibility depends on having the right local legal and tax structure.

Transfer pricing is where this becomes most technically important. If a US company builds a 40-person AI engineering hub in Poland, it may eventually need to document how value is created, who owns the IP, which entity bears risk, and how costs and returns are allocated across the group.

The question of BEPS 2.0 could have popped into your mind, considering the context. From my experience, this is usually not the immediate concern for companies using EOR to validate a new engineering market. Pillar Two applies to large multinational groups with consolidated revenue of at least €750 million, while Pillar One Amount A is aimed at the large and profitable global enterprises. For most scaling tech companies, the more practical tax question at the EOR stage is PE.

When it comes to the commercial dimension, it is simpler but equally concrete. An EOR cannot open a local bank account in your company’s name, hold local assets, or sign commercial contracts as your legal representative. If those needs appear on the roadmap, entity setup becomes a business infrastructure decision, not just a tax question.

Yet none of these reasons automatically means that you need to rush into entity setup. The right strategy would be to use the services of one of the EOR providers first: validate the tech market, build the engineering team, and launch local operations to assess first results. Once headcount, customer presence, or long-term tax planning make the market strategic, the entity transition can be planned.

If your scaling strategy involves entering one of the tech markets in Latin America or Eastern Europe, Alcor can help you do so compliantly and avoid the risk of a permanent establishment.

As the best EOR for tech startups and scaleups as well as mature companies, Alcor operates through owned legal entities and offers all-in-one operational infrastructure. For you, that means getting:

- In-country legal and payroll expertise with a dedicated Customer Ops Manager, who owns all issues end-to-end,

- Tailored FTE and B2B contracts compliant with the local labor laws,

- 10-day talent onboarding via customized setup,

- Legal shield for PE risk, worker misclassification, payroll, and IP,

- No deposits, FX charges, or hidden costs – one service fee and volume discounts for team growth,

- Plus full-cycle tech recruitment and operational support under one roof.

Fill out the form below and start scaling your engineering team confidently with Alcor.

Questions you can ask AI about EOR and PE risks:

- Can hiring engineers through an Employer of Record create permanent establishment risk for my tech company?

- What activities can turn a remote engineering team into a taxable business presence abroad?

- When should I move from an EOR model to a local entity to reduce PE exposure?

FAQ

Can an EOR eliminate permanent establishment risk entirely?

No. An EOR removes the administrative and employment triggers, such as contracts, local payroll, tax filings, and statutory registrations, that would otherwise create a direct company footprint in the host country. But it cannot override what your employees actually do. If their activities, authority, or location meet the threshold for permanent establishment, the EOR structure won’t prevent a PE finding.

Which employee activities are most likely to create PE risk despite an EOR?

The highest-risk activities are:

- negotiating or concluding contracts locally,

- managing vendor or client relationships with commercial authority,

- performing core revenue-generating work in-country,

- and exercising senior decision-making from a fixed location.

You can avoid PE when hiring internationally by mapping every role against these criteria before hiring, not after the team has been operating for years.

What are the consequences of permanent establishment?

A PE finding triggers corporate tax on profits attributable to the local presence, applied retroactively from the start of the activity. Additional financial penalties, mandatory local registration, and full compliance with host-country employment obligations follow. In some jurisdictions, corporate tax, VAT, and social security come due simultaneously. Double taxation is possible if both countries assert the right to tax the same profits.

When should a company reassess whether to move from an EOR to a local entity?

Reassess when the country becomes a long-term strategic market, when a senior leadership layer is operating in-country, when regulatory or licensing requirements demand a registered entity, or when long-term tax planning (transfer pricing, R&D incentives, local invoicing) makes a subsidiary structurally worthwhile. A permanent establishment risk assessment at each of these inflection points keeps the decision proactive rather than reactive.